How Michigan Funds Local Public Transportation

As the Rapid prepares their next master plan there is a clear desire for new routes, improved frequency, extended service hours, improved frequency, additional weekend service, improved frequency, as well as a desire for the region to consider other modes including light and heavy rail. Between these visions of a robust regional transit system and reality lies multiple obstacles. One of those challenges is cultural and political inertia. That is real. Yet another, more significant IMO, is the less often discussed challenge: funding.

It is important for advocates to understand the current state of public transportation funding in Michigan, at least to know how opaque the current regime is. What follows merits an Extremely Wonky trigger warning, but is as succinct as I believe possible. Here I am only discussing state (Michigan) funding of local transportation operation; ignore capital projects, grant funding, and any federal assistance – which in total contribute little to the operation of local transit service.

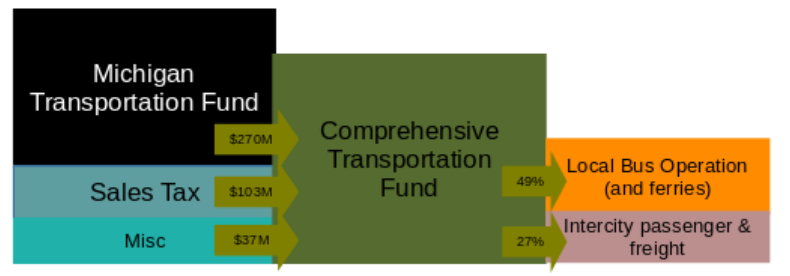

In the state of Michigan a large majority of state funding of not-roads transportation comes via the Comprehensive Transportation Fund (CTF). This is a fund established by section 10b of Public Act 51 of 1951; commonly referred to as just “Act 51”. In any conversation about Michigan transportation funding you will see endless references to Act 51 as this act defines the formula by which the Michigan Transportation Fund (MTF) is distributed. A simple reading of Act 51 indicates that the CTF receives 10% of the revenue of the MTF. It’s not that simple.

In the 2022-2023 fiscal year the MTF’s revenue sources, principally motor fuel sales tax and vehicle registration taxes, generated $~3.7 BILLION dollars of revenue. The CTF received $~270 MILLION dollars; or ~7.5% of MTF revenue. An amount $100 MILLION dollars short of the 10%. This shortfall is due to some allocations which come off the top of the MTF revenues prior to the “10%” calculation being applied.

The second primary source of CTF funding is the auto related sales tax. This is a fun one. The General Sales Tax Act specifies: “not less than 27.9% of 25% of the collections of the general sales tax imposed at a rate of 4%” on the sale of motor vehicles and related goods are to be deposited in into the CTF. However, in practice, this level of funding from the auto related sales tax has never occurred. The Michigan Department of Treasury does not track sales tax by product category but only by the type of retailer. This means that sales of products by auto dealerships and service stations are applied to the CTF formula but the sales of auto parts, motor oil, etc.. at a general retail are not. Additionally, as a sales tax, no revenue is captured from leased vehicles as there is no sale. Also - yes, there is more - while the Michigan sales tax is prescribed in the state constitution the 27.9%-of-25% is merely statutory; as statutory the state legislature can preempt this allocation, and they do.

In total the CTF’s revenue for the 2022-2023 fiscal year was $~411 MILLION dollars; $270 MILLION from the MTF, $103 MILLION from the auto-related sales tax, and $37 MILLION from interest on carrier balances and other sources.

The largest pay out from the CTF is to “Local Bus Operating Assistance '' (LBOA) which is funding distributed to the state’s ~80 public transportation authorities. The Rapid / Inter-Urban Transit Partnership (ITP) is one of these recipients. The amount distributed by the CTF in 2022-2023 to local bus operators was $~201 MILLION [49% of the CTF, ~5% of the MTF]. The guideline in Act 51 for the distribution of funds to local bus operators is: Urban bus operators can apply for CTF funds up to 50% of their eligible expenses, rural transit operators can apply for up to 60%. However, bus operators established before the 1996-1997 fiscal year have a special funding floor relative to the ratio of CTF funds those agencies received in the fiscal year ending in 1989. Currently those legacy agencies are those of the city of Ionia, Berrien County, and Cass county - and sort of the Detroit Transportation Corporation (DDOT). The Michigan Department of Transportation (MDOT) treats the DDOT and the Regional Transportation Authority of Southeast Michigan as a combined unit when calculating funding distributions although the RTA was not created until 2012. If this seems odd, or unfair to other regions of the state, ... well, they don’t count all the expenses of the RTA as eligible for CTF matching.

Confused yet? There’s more. Ferries in Michigan are buses, in that ferry operators can apply for 50% match of their eligible expenses against the Local Bus Operating Assistance fund. There are four ferry operators in the state of Michigan: the Beaver Island Transportation Authority, the Ironton Ferry (Charlevoix County), the City of machican Island, and the Eastern Upper Peninsula Transportation Authority.

All these bus and ferry operators can apply for their respective percentage matches of their qualifying expenses. However, with a balance of $~200 MILLION the LBOA does not come close to matching the funding applied for. In order to scale the available funds to the qualifying expenses MDOT pro-rates the CTF match, attempting to equalize with the aforementioned 50% urban / 60% rural match specified in Act 51. This ratio in the 2022-2023 fiscal year was a match of 29.2% for urban transportation authorities and 35% for rural transportation authorities. This prorated match continues to decline. In the 2000-2001 fiscal year the CTF matched 38.1% urban and 45.7% of rural eligible expenses for non-legacy non-ferry-operator transportation authorities.

Additionally, other line items have been added or adjusted in the distribution of CTF funds. In the fiscal year 2012-2013 the LBOA was 64% of the CTF expenditure, in 2022-2023 the LBOA is 49% of the CTF. Most significantly the allocation for intercity passenger and freight has increased in that same time from 10% to 27%. Funds allocated elsewhere come at the expense of local bus operations.

It is entirely within the purview of the state legislature to augment CTF funding of transit operations from the General Fund. That has not happened in recent decades.

This steady decline of state funding increases the pressure on local transportation providers to lean more heavily on the only significant sources of funding available to them: local property tax revenues and fares. State funding now accounts for, on average, a third of the operating funding for local transportation authorities. Next newsletter I plan to discuss local funding and the comparison of local funding of transit across the state of Michigan.

-Adam Williams